Unpacking the Global Gateway’s Financial Structure: A Critical Look at its Development Logic

Unpacking the Global Gateway’s Financial Structure: A Critical Look at its Development Logic  2026 Corporate Sustainability Due Diligence Directive – The amendment process and its impact

2026 Corporate Sustainability Due Diligence Directive – The amendment process and its impact  NATO’s Strategic Recalibration in the Cognitive Era

NATO’s Strategic Recalibration in the Cognitive Era  Fast Fashion, Fast Waste: Investigating the intersection of human health and environmental injustice.

Fast Fashion, Fast Waste: Investigating the intersection of human health and environmental injustice.

Written by: Finn Marten, Kiel University & Kiel Institute for the World Economy*

Edited by: Lucia Torlai

Introduction

The sanctions against Russia, imposed following its 2022 invasion of Ukraine, represent one of the most coordinated economic sanction campaigns in modern history. To prevail against Moscow’s war efforts, a coalition of sanctioning countries – led by the European Union, the United States, and the United Kingdom – aims to curb its ability to finance military spending by isolating Russia from the world economy. The European Union, in particular, is constantly adding new measures to its already unprecedented sanction regime, while cutting economic dependencies with Russia and providing financial, military, and humanitarian aid to Ukraine. Have these sanctions truly delivered the desired impact, or has Russia found ways to evade them? This article explores two key loopholes in the EU’s sanction regime: Russia’s circumvention of the price cap on energy exports and the rise of transshipments via Central Asia and the Caucasus.

Since 2022, the EU has drastically reduced its imports of Russian oil and gas, while rising economies like China and India have rapidly increased their purchases. To prevent Russia from financing military spending with its new revenues, the coalition implemented a global price cap on Russian oil and petroleum exports. Because the price cap is enforced via bans on maritime services like insurance to non-compliant vessels, Russia now operates a “shadow fleet” of dangerously old vessels without insurance to sell above the price cap. A second potential sanction loophole is transshipments, where uncontrolled exports flow through third-party economies into Russia. Exports of EU member states to Central Asia and the Caucasus increased severely after the Russian invasion, including mostly machinery and vehicles – goods under export restrictions.

This article will assess if such loopholes endanger the success of the EU sanctions. Therefore, I first review the sanctions imposed since February 2022 to study the macroeconomic impact on the Russian economy. Second, I will then analyze the rise of transshipments and the price cap circumvention. I will also propose strategies to strengthen the EU’s sanctions regime moving forward.

EU sanctions since February 2022

Sanctions are established tools of economic statecraft, offering the opportunity of leveraging economic relations for geopolitical gains (Blackwill and Harris, 2016). After a steady increase in active sanctions per year, 2022 marked an all-time high in newly introduced sanctions despite their low general success rate of only 30% (Syropoulus, 2024). Economic literature finds that sanctions success depends on the economic size and connectedness of the target (Itskhoki and Ribakova, 2024), as well as the sanctioning coalition’s size and economic cost (Chodry et al. 2024).

Since February 2022, the EU (2024a & 2024b) has implemented 14 packages of sanctions to limit Russia’s ability to finance its war in Ukraine. Economic measures aim to weaken Russia’s economy by targeting six key sectors – trade, finance, energy, transport, services, and defence and technology. Trade sanctions include import and export bans on raw materials, such as iron or steel, and luxury goods. Furthermore, trade sanctions cover military and dual-use goods, which can be used for civilian and military purposes, like parts for vessels, aircraft, or trailers. Energy trade is restricted by a price cap for Russian seaborne exports of crude oil and petroleum. The EU closed its airspace and ports for Russian aircraft and vessels and issued a ban on transport-related services. The supply of further key services like legal advisory or credit rating is also sanctioned. Lastly, financial sanctions impact many sectors by restricting Russia’s ability to access global capital and financial markets. Among the first sanctions in early 2022, the EU and its partners forced Belgium-based SWIFT, the leading provider for financial messaging, to cut selected Russian banks off from its network, reducing Russia’s ability to conduct cross-border financial transactions crucial for international trade. Additionally, the EU and its partners froze €260 billion in assets from the Central Bank of Russia alongside assets of selected policymakers, oligarchs, and military officials, including those of Russian President Vladimir Putin (EU, 2024c).

The Russian Economy

The primary goal of the EU sanction regime is to stop Russia from financing its war in Ukraine by weakening its economy. At an aggregated level, Russian GDP initially fell by 4.4% after February 2022 but recovered shortly afterwards, driven by a substantial militarisation of the economy through large official spending and military production (Gorodnichenko et al, 2024). War-related industries grew production by 60% since autumn 2022, compared to negligible production growth in other manufacturing sectors. Russia’s 2023 military spending increased by 24% to roughly €100 billion, which corresponds to 5.9 % of its GDP (SIPRI, 2024). For comparison, the 2022 share in the EU 2022 was only 1.3% (Eurostat, 2023). Official state budget drafts published by the Russian State Duma in September 2024 reveal plans to increase defence spending to roughly €130 billion or 6.3% of GDP, marking the highest level since the Cold War (Reuters, 2024). A recent report by Wolff et al. (2024) also estimates that Russia has increased its production rates for key weapon systems drastically (215% for tanks, roughly 150% for artillery, and even 475% for loitering munition). Thus, Russia could produce all the military equipment of Germany, Europe’s largest economy, in only six months.

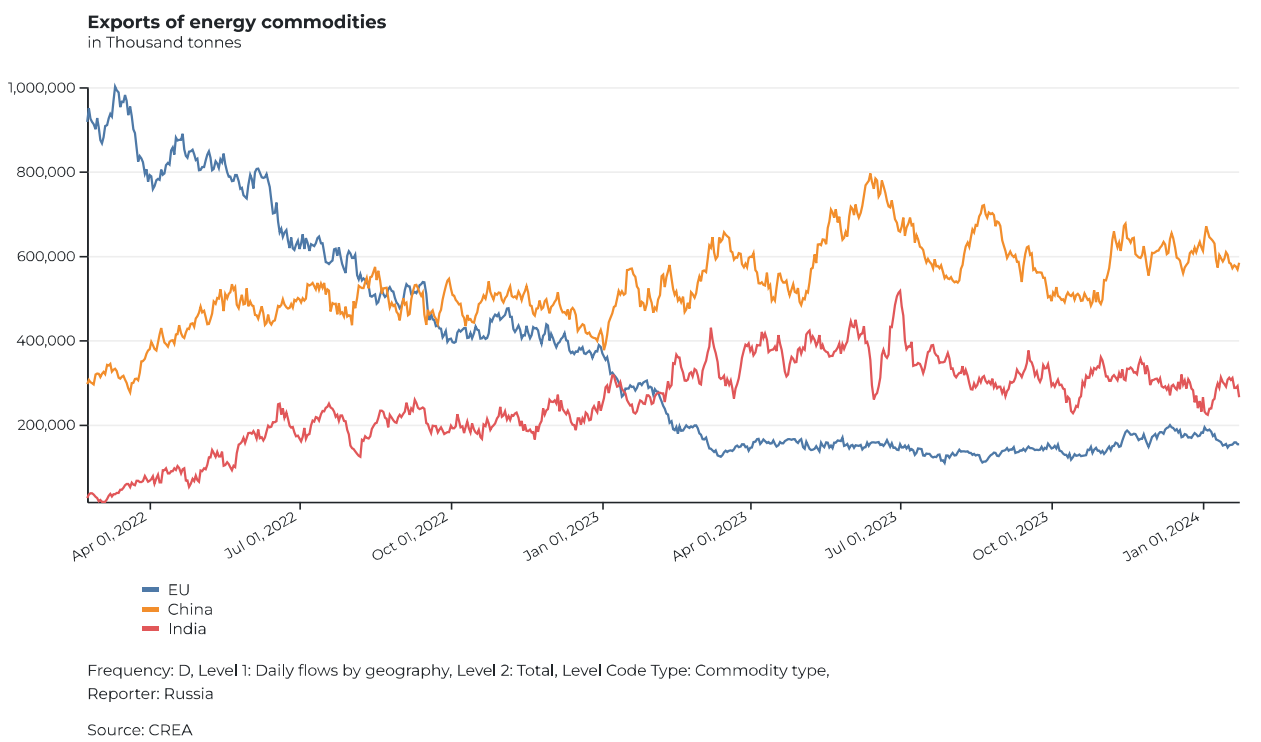

Russia finances the huge costs of the war largely through its revenue from energy exports (Gorodnichenko et al, 2024). While Figure 2 shows that the EU successfully reduced its dependence on Russian energy, it also depicts how the slow rollout of sanctions allowed Russia to redirect energy exports to new destinations. For instance, oil import bans were not implemented until December 2022. By then, non-coalition countries, such as China and India, had already increased their energy imports from Russia. Similar dynamics also apply to Russian trade in other commodities (Russia Monitor, 2024). Combined with soaring export prices, Russian oil and gas revenues remained at high levels, accounting for 32% of all government revenues (Yermakov, 2024). Thus, targeting Russian revenues from energy exports, the EU sanctions have aimed the right way but failed to isolate the Russian economy due to slow implementation and weak enforcement while military production is temporarily boosting Russia’s official GDP figures (Itskhoki and Ribakova, 2024).

Figure 2: Exports of Russian energy commodities in Thousand tonnes to the EU, China, and India since February 2022. Source: Russia Monitor developed by Vienna Institute for International Economic Studies, ifo Institute for Economic Research, Kiel Institute for the World Economy and Austrian Institute of Economic Research(2024)

Transshipments

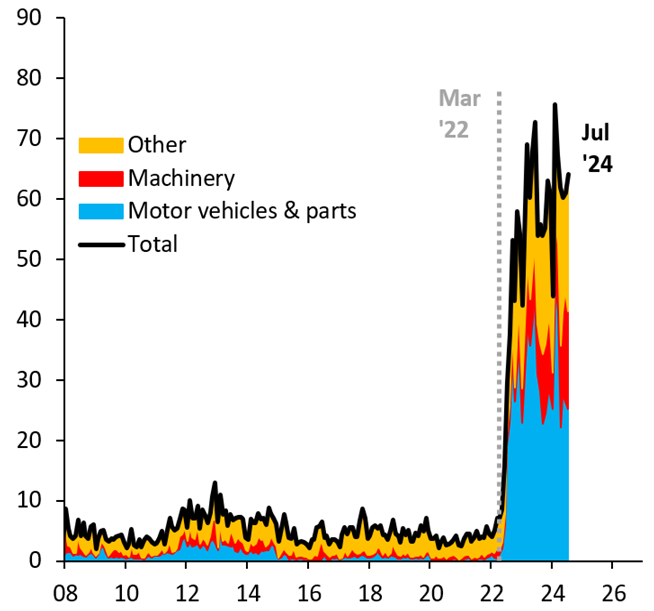

Many countries did not join the sanction coalition and continued trading with Russia, allowing the rise of transshipments to threaten sanction success. Just half a year after the invasion European Commission president Ursula von der Leyen (2022) addressed reports about Russia importing electronic devices like washing machines through third-party states to retrieve banned electronic parts, for weapons manufacturing. Recent trade data shows such third-party transshipments. Exports from large EU economies to Central Asia and the Caucasus soar in value since the start of the Russian invasion (Brooks, 2024c). In particular, the value of German and Italian exports to countries like Kyrgyzstan, Kazakhstan, Armenia, and Turkey has increased by large margins (Brooks, 2024b). But do those Russian imports via non-coalition economies include sanctioned goods? Figure 3 shows the decomposition of monthly exports of goods to Kyrgyzstan by Germany. The share of motor vehicles, parts, and machinery has increased severely since March 2022. Although such data is no direct evidence for systematic sanction evasion, it justifies reasonable concern that transshipments can include EU-sanctioned goods usable for military purposes.

Figure 3: Decomposition of Germany’s monthly exports of goods to Kyrgyzstan in € million. Data from German Statistical Office. Source: Brooks (2024b)

Although likely overstated due to soaring inflation and far from a causal relation, transshipments are in line with findings on the fragmentation of the world economy. Since the Russian invasion global trade patterns have shifted to geopolitically aligned trade blocs, fostering the emergence of “connector economies” that increase trade with both geopolitical blocs due to their neutrality (Gopinath, 2024). Although small when compared to the reductions in EU-Russian trade since 2022, Brooks (2024b) estimates that combined with other export increases from non-EU countries, the rise in transshipments via Central Asia and the Caucasus could substantially offset the direct trade sanction effects.

Publicly available data does not allow further analysis since it is aggregated over product categories and only published with delays. Because transshipments are especially visible for certain EU members, as a first step, their national customs agencies could launch detailed investigations to examine indirect trade of banned goods and separate price effects. On the other hand, targeting transshipments with further trade sanctions would inflict low economic costs as transshipments constitute only a small part of EU exports (Brooks, 2024b). Furthermore, to detect the emergence of new destinations for transshipments, the EU might implement coordinated monitoring of its member’s customs data.

The Oil Price Cap

The second loophole is the circumvention of the oil price cap. Although implemented only with a small (G7) coalition, the price cap leverages international dependency on maritime service providers in coalition jurisdiction, a concept called “Weaponized Interdependence” (Farrell and Newman, 2019). This allows targeting seaborne energy exports to non-coalition countries, forcing them into compliance, boosting the price cap effectiveness, and ultimately lowering Russia’s ability to finance war through energy revenues (Johnson et al. 2023). Figure 3 plots the “Urals discount”, the difference between Russian and world market oil prices since 2022. While Russia is forced to sell at high discounts, the delayed recoveries after price cap implementation and enhancement policies suggest circumvention.

Figure 4: Urals discounts average – Price difference from Brent Price (5-day rolling average). Source: Johnson & Wolfram (2024)

In addition to exports via its state-owned Sowkomflot vessels, Russia has assembled a fleet of ageing tankers under hidden ownership, to sell oil above the price cap by operating without insurance despite the high oil-spill risks of the old vessels (Brooks, 2024a). Cargo switches at sea aim to further disguise the origin of oil exports to sell above the price cap (Su, 2024).

Although designed to never fully stop Russian energy exports due to EU dependency and price effects, the price cap could achieve higher discounts through decisive enforcement. First, the EU could ban the sale of tankers to undisclosed buyers since many sales involve vessels from Greece’s large tanker fleet, placing them under EU jurisdiction (Brooks, 2024a). Such a ban could turn out particularly effective given the short expected lifespan of shadow fleet vessels. Second, sanctions on Russia’s official state-owned tanker fleet could be extended. Although only certain state-owned Sowkomflot tankers are so far sanctioned, Russia is already rotating exporting vessels, potentially due to strains from high usage (Brooks and Harris, 2024). Thus, EU sanctions on more Sowkomflot tankers would increase the pressure to comply with the price cap via commercial tankers. Third, due to the high environmental risk of shadow fleet tankers, EU members could also create a mechanism to control oil tanker insurance when they navigate the Baltic Sea. Such a mechanism could effectively exclude the largest part of the shadow fleet from operating in one of Russia’s key oil exporting routes (Kennedy, 2024).

Conclusion

Russia’s military spending plans and actions on the battlefield in Ukraine show its willingness to bear the current economic cost of the sanction regime. However, in order to put further pressure on export revenues and Russia’s ability to finance its military production, the EU can enhance the enforcement of the oil price cap. Moreover, it should investigate if the transshipments from EU countries to Russia systematically include dual-use goods. With rising defence budgets and debates about EU debt, a major advantage of the proposed policies is their low economic cost. Strengthening the sanctions and acting against the deadly war waged by Russia seems to depend mostly on the political will of the EU and its members.

Notes: If not indicated otherwise, all information on EU sanctions was taken from online EU overview resources such as their sanctions timeline (EU, 2024b) and the Explained section (EU, 2024a).

*The author is a student at Kiel University and a student research assistant at the Kiel Institute for the World Economy. The responsibility for the contents of this commentary rests only with the author and does not represent the views and work of Kiel University or the Kiel Institute for the World Economy. Please feel free to get in touch for suggestions and comments: finn.ma7@gmail.com

References:

Blackwill, R. and Harris, J. (2016). War by other Means. Council on Foreign Relations, Harvard University Press, ISBN 978-0-674-73721-1

Brooks, R. (2024a). Threats to global economic security: Weak sanctions implementation and high debt. Brookings Commentary, 04. https://www.brookings.edu/articles/threats-to-global-economic security-weak-sanctions-implementation-and-high-debt/

Brooks, R. (2024b). Transshipments from Germany to Russia. Brookings Commentary, 09. https://www.brookings.edu/articles/transshipments-from-germany-to-russia/

Brooks, R. (2024c). Transshipments from the EU to Russia. Brookings Commentary, 09. https://www.brookings.edu/articles/transshipments-from-the-eu-to-russia/

Chowdhry, S., Hinz, J., Kamin, K., & Wanner, J. (2024). Brothers in arms: the value of coalitions in sanctions regimes. Economic Policy, 39(118), 471–512. https://doi.org/10.1093/epolic/eiae019

EU – Council of the EU and the European Council. (2024a). EU sanctions against Russia explained.https://www.consilium.europa.eu/en/policies/sanctions-against-russia/sanctions-against-russia-explained/

EU – Council of the EU and the European Council. (2024b). Timeline – EU sanctions against Russia. https://www.consilium.europa.eu/en/policies/sanctions-against-russia/timeline-sanctions-against-russia/

EU – Council of the EU and the European Council. (2024c). Immobilised Russian assets. https://www.consilium.europa.eu/en/press/press-releases/2024/02/12/immobilised-russian-assets-council-decides-to-set-aside-extraordinary-revenues/

Eurostat. (2023). Government expenditure on defence. https://ec.europa.eu/eurostat/statistics explained/index.php?title=Government_expenditure_on_defence

Farrell, H., & Newman, A. L. (2019). Weaponized Interdependence: How Global Economic Networks Shape State Coercion. International Security, 44(1), 42–79. https://doi.org/10.1162/isec_a_00351

Gopinath, G. (2024). Changing Global Linkages: A New Cold War? IMF Working Papers: Vol. 2024. International Monetary Fund. https://doi.org/10.5089/9798400272745.001

Gorodnichenko, Y., Korhonen, I., & Ribakova, E. (2024). Policy Insight 131: The Russian economy on a war footing: A new reality financed by commodity exports. CEPR Policy Insight(131). https://cepr.org/publications/policy-insight-131-russian-economy-war-footing-new-reality-financed commodity-exports

Harris, B., & Brooks, R. (2024). Strains on the Sovcomflot oil tanker fleet. Brookings Commentary, 08. https://www.brookings.edu/articles/strains-on-the-sovcomflot-oil-tanker-fleet/

Itskhoki, O., & Ribakova, E. (2024). The economics of sanctions: From theory into practice: BPEA Conference Draft, Fall. Brookings Papers on Economic Activity. https://www.brookings.edu/wp content/uploads/2024/09/6_ItskhokiRibakova.pdf

Johnson, S., Rachel, L., & Wolfram, C. (2023). Design and implementation of the price cap on Russian oil exports. Journal of Comparative Economics, 51(4), 1244–1252. https://doi.org/10.1016/j.jce.2023.06.001

Johnson, S., & Wolfram, C. (2024). Strengthening Enforcement of the Russian Oil Price Cap. Brookings Policy Brief, 07. https://www.brookings.edu/wp-content/uploads/2024/07/20240701_WolframJohnson_Sanctions.pdf

Kennedy, C. (2024). Making the Baltic a “shadow-free” zone: A proposal to reduce Moscow’s shadow fleet with minimal risk of litigation, escalation, or market disruption. Brookings Policy Brief, 07. https://www.brookings.edu/wp-content/uploads/2024/07/20240701_Kennedy_Sanctions.pdf

Reuters (2024). Russia hikes 2025 defence spending by 25% to a new post-Soviet high https://www.reuters.com/world/europe/russia-hikes-national-defence-spending-by-23-2025-2024-09-30/

Russia Monitor. (2024). Vienna Institute for International Economic Studies, ifo Institute for Economic Research, Kiel Institute for the World Economy, Austrian Institute of Economic Research. https://rus-monitor.wiiw.ac.at/

SIPRI. (2024). Global military spending surges amid war, rising tensions and insecurity. https://www.sipri.org/media/press-release/2024/global-military-spending-surges-amid-war-rising tensions-and-insecurity

Su, S. (2024). Ships Still Switch Russian Oil Off Greece Despite Navy Drills. Bloomberg. https://www.bloomberg.com/news/articles/2024-09-20/ships-still-switch-russian-oil-off-greece-despite-navy-drill

Syropoulos, C., Felbermayr, G., Kirilakha, A., Yalcin, E., & Yotov, Y. V. (2024). The global sanctions database–Release 3: COVID-19, Russia, and multilateral sanctions. Review of International Economics, 32(1), 12–48. https://doi.org/10.1111/roie.12691

von der Leyen, U.(2024). Keynote by the President at the Tallinn Digital Summit. https://ec.europa.eu/commission/presscorner/detail/en/SPEECH_22_6063

Wolff, G., Burilkov, A., Bushnell, K., & Kharitonov, I. (2024). Fit for war in decades: Europe’s and Germany’s slow rearmament vis-a-vis Russia. Kiel Report, 09(1). https://www.ifw kiel.de/publications/fit-for-war-in-decades-europes-and-germanys-slow-rearmament-vis-a-vis-russia 33234/

Yermakov, V. (2024). Follow the Money: Understanding Russia’s oil and gas revenues. Oxford Energy Comment, 03. https://www.oxfordenergy.org/wpcms/wp-content/uploads/2024/03/Follow-the Money-Russian-Oil.pdf