High-speed rail as a strategic infrastructure: a review of the EU’s high-speed rail vision within the TEN-T framework

High-speed rail as a strategic infrastructure: a review of the EU’s high-speed rail vision within the TEN-T framework  Dissent at the centre: protest policing in the EU’s capital

Dissent at the centre: protest policing in the EU’s capital  Unpacking the Global Gateway’s Financial Structure: A Critical Look at its Development Logic

Unpacking the Global Gateway’s Financial Structure: A Critical Look at its Development Logic  2026 Corporate Sustainability Due Diligence Directive – The amendment process and its impact

2026 Corporate Sustainability Due Diligence Directive – The amendment process and its impact

Written by Dianne Smits

EO Writer & Product developer at KernTec GmbH

Abstract

In February 2026, the Corporate Sustainability Due Diligence Directive (CSDDD), regulating sustainable development of companies, was amended in a very short time, with limited consultation of experts and stakeholders. A probable reason for this is pressure and potential threats from big corporations, and important players in the supply chain of fuels. The changes that were made might form a threat towards achieving the 2050 climate targets. In addition, the way the amendments were introduced is a clear reflection of the turbulent political environment that has been unfolding, and set an alarming precedent for future rulemaking in the European Union.

Keywords

Corporate Sustainability Due Diligence Directive — Amendment — Climate targets — Corporate lobby

1. Introduction: Why the 2026 CSDDD amendment matters for EU climate governance

In February 2026, the European Union amended the Corporate Sustainability Due Diligence Directive (CSDDD) through the Omnibus I simplification package, introducing substantial changes to one of its central sustainability instruments. The amendment matters not only because it alters the obligations imposed on large companies, but because it also tests the coherence of the EU’s extended sustainability governance at a moment when climate ambition increasingly depends on credible implementation.

That wider framework is well established. Under the European Climate Law, the European Union is legally committed to reducing greenhouse gas emissions by at least 55% by 2030, reaching a 90% reduction by 2040, and becoming climate-neutral by 2050 (European Commission, n.d.). Yet these objectives cannot be realised through public policy alone. They also depend on the extent to which corporate actors are required to identify, prevent, and limit the environmental harms that can arise in their operations and value chains.

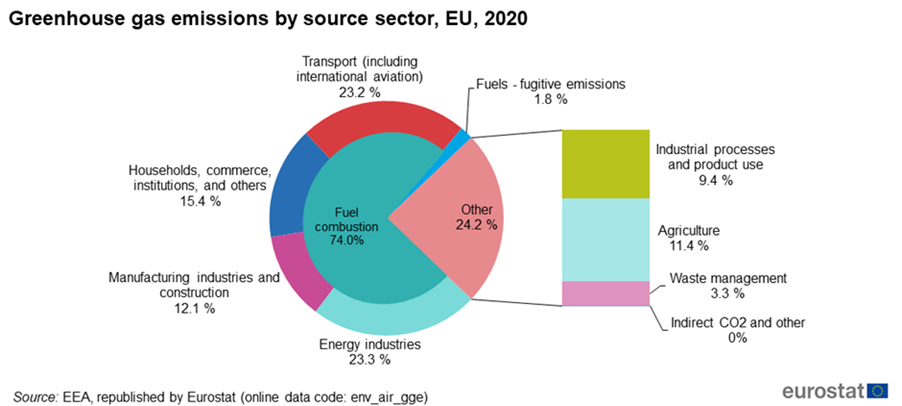

The CSDDD was designed to connect corporate conduct more closely to the Union’s environmental and social objectives (Corporate Sustainability Due Diligence, n.d). By introducing due diligence obligations for large companies, it sought to connect corporate conduct more closely to the European Union’s environmental and social objectives (Directive – EU – 2024/1760 – EN – EUR-Lex, 2024). Figure 1 illustrates that business activity is still a major source of emissions in the EU, which helps explain why corporate due-diligence obligations matter within the wider climate-governance framework (Eurostat, 2025). With this information, the 2026 amendment raises a fundamental policy question: can the EU keep claiming to show climate leadership while simultaneously weakening one of the mechanisms created to make that leadership operational?

Figure 1. Business activity as a primary source of greenhouse gas emissions in the European Union

Source: Adapted from “The European Union has cut greenhouse gas emissions in every sector – except this one” (World Economic Forum, 2025), based on Eurostat data.

2. Policy Description

The CSDDD forms part of the EU’s wider sustainability and climate-governance framework, which was strengthened by the 2021 European Climate Law (EUR-LEX – L:2021:243:TOC – EN – EUR-LEX, 2021). The directive entered into force on 25 July 2024 and established obligations for large companies to identify, prevent, mitigate, and account for adverse human rights and environmental impacts within their supply chains (Directive – EU – 2024/1760 – EN – EUR-Lex, 2024).

The directive originally applied to EU companies with more than 1,000 employees and a net worldwide turnover exceeding 450 million euros, as well as to non-EU companies generating more than 450 million euros turnover within the Union. Its purpose was to require large firms to map their supply chains and improve transparency, including corporate activity more within the Union’s wider effort to align economic, financial and corporate behaviour with sustainability objectives (Corporate Sustainability Due Diligence, n.d.). The CSDDD is closely linked to the CSRD, the Corporate Sustainability Reporting Directive, which complements it by requiring companies to disclose relevant sustainability information (Byrne, 2025).

Timeline of the CSDDD amendment

The timeline below summarises the main milestones of the original directive and its 2026 amendment (European Commission, 2026):

2024 – Entry into force of the CSDDD

February 2026 – Adoption of the Omnibus I amendment

2028 – Deadline for Member State transposition

2029 – Application of the amended directive to companies in scope

Omnibus I – What changed?

As stated, the changes that were applied to the 2026 version of the CSDDD watered down its effect and made it less able to fulfill its goal of including corporate institutions in the sustainability targets of the EU. The main points of the CSDDD that were affected are;

Scope

The amendment significantly narrowed the directive’s scope. The threshold for EU companies was raised from 1,000 employees and 450 million euros turnover to 5,000 employees and 1.5 billion euros net worldwide turnover. Similar changes were introduced for non-EU companies. As a result, around 75% of firms that would initially have been covered by the directive are now excluded (Kincaid, 2026).

Transition-plan obligation

Under the initial directive, companies were required to “adopt and put into effect a transition plan for climate change mitigation” (Directive – EU – 2024/1760 – EN – EUR-Lex, 2024). In the amended version, the obligation to actually put such a plan into effect was removed. Companies must still produce plans, but the directive no longer requires that those plans be meaningfully implemented in ways that achieve alignment with the EU’s climate goals (Stares & Gray, 2025).

Enforcement and liability

The amendment also weakened enforcement mechanisms. The maximum financial penalty for non-compliance was reduced from 5% to 3% of net turnover (Omnibus I – the European Union Concludes CSDDD and CSRD Reforms, 2026). In addition, the earlier EU-wide approach to civil liability was replaced by greater reliance on national enforcement and litigation frameworks, leaving more room for divergence across the Member States (Stares & Gray, 2025).

3. Policy Problem

The central policy problem created by the 2026 amendment is that simplification may reduce regulatory coverage and weaken enforcement in ways that undermine market transparency, implementation equality, and the credibility of the EU’s longstanding sustainability. This is because the CSDDD was designed as an essential mechanism to deal with the Union’s climate and sustainability objectives, weakening it risks hollowing out the practical effectiveness of the broader structure which it is part of.

4. Policy Research and Analysis

4.1 Reduced transparency and narrower market coverage

The first likely effect of the amendment is reduced transparency across value chains. By excluding a substantial share of firms from the directive, the amended framework limits the amount of sustainability-related information that can be obtained, monitored, and compared across markets. What is weakened is therefore not only legal scope, but also the informational basis on which investors, regulators, and firms themselves rely when gathering data on corporate sustainability (Lefebvre Du Prey & Kerkvliet, 2025).

This has direct consequences for implementation. Investors may find it more difficult to obtain the data necessary to allocate capital in line with sustainability objectives, while companies that remain within the directive’s scope may struggle to obtain reliable information from suppliers and partners that are no longer covered (Lefebvre Du Prey & Kerkvliet, 2025). In this sense, narrowing the directive may also reduce its effectiveness for the firms that continue to fall under it (Libert, 2025).

4.2 Fragmented enforcement across Member States

A second likely effect concerns implementation coherence. By shifting responsibility for liability and enforcement more decisively to national systems, the amendment increases the likelihood that compliance standards will vary across Member States. Such divergence risks the production of a fragmented regulatory landscape in which the meaning and practical force of the directive differ depending on jurisdiction.

That fragmentation is not merely procedural. It may create incentives for companies to locate activities in Member States where enforcement is weaker, thereby encouraging social and environmental dumping (EU: Study Finds Effective CSDDD Would Bring Significant Economic Benefits for Europe & Beyond – Business and Human Rights Centre, 2025). In a policy area where the Union seeks to establish common standards for responsible corporate conduct, the differences in enforcement risks undermine both fairness and effectiveness.

4.3 Competitive disadvantage for early movers

A third effect is the competitive disadvantage that may arise for firms that had already started adjusting to the original directive. Some companies invested early in sustainability strategies, due diligence systems, and more transparent value-chain management in anticipation of stricter obligations. Under the amended framework, competitors that delayed such investments may now face weaker requirements or no direct obligations at all (European Commission, 2026).

This creates an unequally divided incentive structure. Firms that adapted their sustainability policies more proactively to be in line with the European Union’s sustainability agenda may be facing higher costs than competitors who did not. Over time, such an outcome may discourage early adjustment and weaken the credibility of future sustainability regulation as a driver of long-term corporate change. A possibility would even be that this delayed action is extended to other progressive policies.

4.4 Amendment process and stakeholder influence

The implications of the amendment are not only about the contents of the directive, but also the process itself. Although the amendment was presented as a simplification measure intended to reduce regulatory obstacles and support competitiveness, the speed of the process and the limited consultation of experts cause concerns about procedural legitimacy.

Reporting from Brussels suggests that ordinary deliberative safeguards were weakened in the rush to amend the directive. Wetzels (2026), writing for Follow the Money, argues that the bypassing of impact assessments and the narrowing of consultation weakened procedural integrity. Similar concerns are raised by De Leth (2025), specifically about the influence of multinational corporate actors from sectors linked to oil, gas, and extractive industries. In addition, an open letter was sent to EU leaders by the United States and Qatar, stating that “the CSDDD, as it is worded today, poses a significant risk to the affordability and reliability of critical energy supplies for households and businesses across Europe and an existential threat to the future growth, competitiveness, and resilience of the EU’s industrial economy.” (U.S. Energy Secretary And Qatari Energy Minister Send Letter to EU Regarding Proposed Corporate Climate Regulations, 2025).

These concerns should be treated with care. It is difficult to attribute a policy outcome to a single causal force. Still, the process itself appears to have generated a legitimate concern that urgency and selective access may have outweighed broad-based, evidence-led consultation. For an EU that often defines its regulatory legitimacy through procedure, that perception is politically significant.

4.5 Competitiveness and the EU’s long-term position

The amendment was justified partly because it should prevent the directive from endangering the Union’s competitiveness. Yet the Commission’s own climate reporting challenges the argument that stronger sustainability regulation necessarily undermines growth and competitiveness. In the Climate Action Progress Report 2024, the Commission argues that the European Union has significantly reduced greenhouse gas emissions while continuing to expand economically, pointing to a long-term decoupling between emissions and growth (Directorate-General for Climate Action, 2024).

The report also frames the European Green Deal as a competitiveness strategy rather than a constraint upon it. Investments in clean technologies, energy efficiency, and reduced fossil-fuel dependence are presented as drivers of resilience and of toughness (Directorate-General for Climate Action, 2024). In that sense, the question is not whether competitiveness matters, but which model of competitiveness the EU seeks to pursue. If competitiveness is understood in short-term deregulatory terms, the amendment seems logical. If it is understood as long-term economic resilience and autonomy, weakening the CSDDD becomes harder to defend.

5. Policy Recommendations

While reversing the amendment may not be feasible, several recommendations could strengthen the current framework. To start, the EC could streamline the enforcement of the directive in all member states to prevent environmental dumping. Civil liability might be a step too far back to the initial directive, but guidelines of the Commission on the enforcement could minimize the difference between member states. Another point would be to make it possible for companies to change their initial sustainability policies that were made before the amendment of the directive. The risk of endangering the 2050 climate target achievement increases by doing so, but it makes sure that early adopters of the policy are not punished. By keeping early adopters to higher standards, a precedent of not adopting sustainability strategies until it is absolutely impossible to avoid them might be set, and this should be avoided to prevent even more setbacks and resistance from companies to be actively involved in achieving climate targets. And recommended would be to give the companies that are currently subject to the CSDDD more leverage to make other companies they work with increase the transparency of their operations. By only involving a few big companies in the directive, it might make it even more difficult for them to obey the requirements, as there might be smaller competitors who are able to do business with companies in the supply chain who do not comply with the set sustainability standards. Giving bigger companies some sort of leverage might enable them to actually comply with the CSDDD. For this to work, the requirement for companies to make a plan which is designed to make them comply with the requirements in the Paris Agreement is necessary. Otherwise, even if the company would be required to stop working with a business that is unable to comply with the set standards, which they are not under the amended version, the company that does not meet sustainability requirements could start working with another, smaller, company. The company that is subject to the CSDDD has then met the requirements of making a sustainability strategy, it was, however, destined to fail.

Concrete recommendations on the improvement of this amendment are thus;

- The European Commission should issue more detailed enforcement guidance to Member States. Clearer Commission guidance would reduce fragmentation in implementation and help ensure that the directive is applied more consistently across national jurisdictions.

- The European Commission should create adjustment flexibility for early adopters of sustainability strategies. Companies that invested early in compliance with the original directive should be allowed to revise existing strategies so that they are not placed at a structural disadvantage relative to firms now facing weaker obligations.

- The EU legislator should strengthen the leverage of in-scope companies over actors in their value chains. Since fewer firms are now directly covered by the directive, those that remain in scope need stronger legal and contractual tools to require transparency and sustainability improvements from suppliers and business partners.

- The European Commission and co-legislators should reintroduce minimum standards for climate transition planning. Even if the obligation to fully “put into effect” transition plans remains politically contested, the directive should require that such plans meet baseline criteria of credibility, measurability, and alignment with EU climate objectives.

These adjustments could help restore coherence and ensure that the CSDDD continues to contribute meaningfully to the EU’s long-term climate objectives.

6. Conclusion

The 2026 amendment of the CSDDD does more than alter the content and set-up of a single directive. It reveals a broader tension within EU sustainability governance between long-term climate ambition and short-term political pressure for simplification and competitiveness. By narrowing the scope, weakening enforcement, and causing the rise of questions about the amendment process itself, the reform risks undermining one of the Union’s main options for translating climate commitments into corporate accountability.

The issue, therefore, is not only whether the amended directive remains legally functional. It is whether the European Union can keep streamlined policies across its sustainability framework if key instruments are weakened at the point of implementation. If the EU really wants to maintain the credibility of its climate governance, it will need not only to defend ambitious changes, but also protect the regulatory mechanisms that make those changes meaningful in practice.

*Artificial intelligence was used in the preparation of this paper to support language editing and improve clarity and structure. All substantive analysis, interpretation, and conclusions remain the sole responsibility of the author. AI-generated output was critically reviewed, revised, and verified against the original sources.

References

Byrne, D. (2025, December 1). What is the CSDDD? The Corporate Governance Institute. https://www.thecorporategovernanceinstitute.com/insights/lexicon/what-is-the-csddd/

De Leth, D. O. (2025, December 3). The secretive cabal of US polluters that is rewriting the EU’s human rights and climate law. SOMO. Retrieved March 13, 2026, from https://www.somo.nl/the-secretive-cabal-of-us-polluters-that-is-rewriting-the-eus-human-rights-and-climate-law/

Directive – EU – 2024/1760 – EN – EUR-Lex. (2024, June 13). https://eur-lex.europa.eu/eli/dir/2024/1760/oj

Directorate-General for Climate Action. (2024). Progress Report 2024 Climate Action. In European Commission. Publications Office of the European Union. https://climate.ec.europa.eu/document/download/7bd19c68-b179-4f3f-af75-4e309ec0646f_en?filename=CAPR-report2024-web.pdf

EU: Study finds effective CSDDD would bring significant economic benefits for Europe & beyond – Business and Human Rights Centre. (2025, September 29). Business and Human Rights Centre. https://www.business-humanrights.org/en/latest-news/economic-benefits-csddd/

EUR-Lex – L:2021:243:TOC – EN – EUR-Lex. (2021, July 9). EUR-Lex. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ%3AL%3A2021%3A243%3ATOC

European Commission. (n.d.). Climate strategies & targets. https://climate.ec.europa.eu/eu-action/climate-strategies-targets_en

European Commission. (2026, February 26). Directive – EU – 2026/470 – EN – EUR-Lex. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202600470

Eurostat. (2024). Treibhausgasemissionen nach Quellsektor [Dataset]. In Publications Office of the European Union. https://doi.org/10.2908/env_air_gge

Kincaid, C. (2026, January 19). The EU has reached an agreement on Omnibus 1 – what are the key changes to CSDDD and CSRD? Sedex. https://www.sedex.com/blog/eu-omnibus-simplification-package-what-you-need-to-know/

Lefebvre Du Prey, I., & Kerkvliet, S. (2025, July 1). Weakening the EU’s sustainability rules risks damaging competitiveness and growth warn companies and investors. IIGCC. https://www.iigcc.org/media-centre/weakening-eus-sustainability-rules-risks-damaging-competitiveness-and-growth-warn-companies-investors#:~:text=Aleksandra%20Palinska%2C%20Executive%20Director%20of,and%20long%2Dterm%20growth.%E2%80%9D

Libert, J. (2025, February 27). The EU’s sustainability rollback is a retreat disguised as simplification. CEPS. https://www.ceps.eu/the-eus-sustainability-rollback-is-a-retreat-disguised-as-simplification/

Omnibus I – the European Union concludes CSDDD and CSRD reforms. (2026, February 24). Clifford Chance. https://www.cliffordchance.com/insights/resources/blogs/business-and-human-rights-insights/2026/02/omnibus-i-the-european-union-concludes-csddd-and-csrd-reforms.html

Stares, K., & Gray, M. (2025, March 6). The EU Omnibus: resetting the rules on sustainability due diligence. CRS. https://www.charlesrussellspeechlys.com/en/insights/expert-insights/corporate/2025/the-eu-omnibus-resetting-the-rules-on-sustainability-due-diligence/

The European Union has cut greenhouse gas emissions in every sector – except this one. (2025, June 3). World Economic Forum. https://www.weforum.org/stories/2022/09/eu-greenhouse-gas-emissions-transport/

U.S. Energy Secretary and Qatari Energy Minister Send Letter to EU Regarding Proposed Corporate Climate Regulations. (2025, October 22). Energy.gov. https://www.energy.gov/articles/us-energy-secretary-and-qatari-energy-minister-send-letter-eu-regarding-proposed-corporate

Wetzels, H. (2026, March 1). ‘Divide and conquer’: U.S. businesses bully Brussels into weakening supply chain rules. Follow the Money – Platform for Investigative Journalism. https://www.ftm.eu/articles/washington-bullies-brussels-into-weakening-supply-chain-rules-eu-csddd